Global Top 100 PCB Manufacturers in 2025 - Mapping the Powerhouse of Electronics

2024 Global Top 100 PCB Manufacturers: Mapping the Powerhouse of Electronics

Printed Circuit Boards (PCBs) are circuit substrates that form inter-point connections and printed components on general-purpose base materials according to predefined designs. Their primary functions include providing mechanical support for electronic components and enabling electrical connections and signal transmission. As the “motherboard” of electronic devices, PCBs are found in nearly all electronic end products. Their quality directly affects product performance and reliability, and the overall development of the PCB industry has become an important indicator of a nation’s competitiveness in the electronic information sector.

Serving as the “skeleton and nervous system” of electronic components, the PCB industry is a foundational pillar supporting the modern electronics ecosystem. With the rapid expansion of AI computing power, the widespread adoption of new energy vehicles, and the continued rollout of 5G communications, the global PCB industry is undergoing a critical transition—from scale-driven expansion to value-oriented upgrading.

According to NTI, there are approximately 2,800 PCB factories worldwide, of which 116 generate over USD 100 million in annual output. These producers are primarily located in the United States, Japan, South Korea, mainland China, and Taiwan. The top 100 companies recorded a combined revenue of USD 81,992 million, and all companies ranked within the top 100 each exceeded USD 100 million in production value.

Based on revenue rankings, the world’s top 10 PCB manufacturers are: ZD Tech, Unimicron, DSBJ, Compeq, Nippon Mektron, TTM Technologies, Tripod, Nanya PCB, Shennan Circuit, and Ibiden. Among these, seven are Chinese companies—two from mainland China (DSBJ at 3rd and Shennan Circuit at 9th) and five from Taiwan (Zhen Ding Technology, Unimicron, Compeq, Tripod, and Nanya PCB ranking 1st, 2nd, 4th, 7th, and 8th respectively). The remaining three companies are from Japan (Nippon Mektron and Ibiden) and the United States (TTM Technologies).

Today, the global PCB industry has become firmly centered in Asia, with production increasingly concentrated in mainland China. Mainland China’s share of global PCB output value surged from 8.1% in 2000 to 56.0% in 2024, making it the world’s undisputed PCB manufacturing hub.

Below is the list of the top 100 PCB companies globally, organized by 2022 global PCB revenue rankings according to Bosson Research:

|

Rank |

English Name |

Chinese Name |

Business Scope |

Revenue (Million USD) |

|

1 |

ZD Tech |

臻鼎科技 |

PCB |

5,913 |

|

2 |

Unimicron |

欣兴电子 |

PCB |

4,848 |

|

3 |

DSBJ |

东山精密 |

PCB |

3,241 |

|

4 |

Compeq |

华通电脑 |

PCB |

2,637 |

|

5 |

Nippon Mektron |

日本旗胜 |

FPC |

2,545 |

|

6 |

TTM Technologies |

迅达科技 |

PCB |

2,495 |

|

7 |

Trpod |

健鼎科技 |

PCB |

2,270 |

|

8 |

Nanya PCB |

南亚电路 |

PCB |

2,231 |

|

9 |

Shennan circuit |

深南电路 |

PCB+HDI |

2,078 |

|

10 |

Ibiden |

提斐电 |

PCB |

1,907 |

|

11 |

AT&S |

奥特斯 |

PCB |

1,882 |

|

12 |

KBC PCB |

建淄集团 |

PCB |

1,682 |

|

13 |

HannStar |

瀚宇博德 |

PCB |

1,646 |

|

14 |

SEMCO |

STEMCO |

PCB |

1,616 |

|

15 |

Kingwong |

景旺电子 |

PCB+FPC |

1,562 |

|

16 |

Young Poong Group |

永丰集团 |

PCB |

1,523 |

|

17 |

Kinsua |

景硕科技 |

PCB |

1,464 |

|

18 |

Wus Group (TW+CN) |

楠梓电子 |

PCB |

1,415 |

|

19 |

Flexum Technology |

台郡科技 |

FPC |

1,383 |

|

20 |

Shinkp Denshki |

新光电气 |

PCB |

1,345 |

|

21 |

Simmtech |

信泰 |

PCB |

1,313 |

|

22 |

BH Flex |

比艾奇 |

FPC |

1,300 |

|

23 |

Maik |

孕卖电了 |

DCR |

1,273 |

|

24 |

AKM Measville |

安捷利 |

PCB |

1,228 |

|

25 |

Victory Giant |

胜宏科技 |

PCB |

1,171 |

|

26 |

LG Innotek |

伊诺特 |

PCB |

1,162 |

|

27 |

Gold circuit |

金像电子 |

PCB |

1,133 |

|

28 |

Daeduck Group |

大德 |

PCB |

1,032 |

|

29 |

Sz Suntak |

崇达技术 |

PCB |

872 |

|

30 |

Nitto Denko |

日东电工 |

PCB |

872 |

|

31 |

SZ Fast Print |

深圳兴森快捷电路 |

PCB |

795 |

|

32 |

Tahwan Techvest (TPT) |

志超科技 |

PCB |

733 |

|

33 |

Fujikura |

仓电子 |

PCB |

733 |

|

34 |

Sumitomo Denko |

住友电工 |

PCB |

716 |

|

35 |

Aoshikan |

奥士康 |

PCB |

678 |

|

36 |

Olympic |

世运电路 |

PCB |

658 |

|

37 |

CMK |

中央铭板 |

PCB |

638 |

|

38 |

Chin Poon |

敬鹏 |

PCB |

607 |

|

39 |

Unitech |

展华 |

PCB/HDI |

601 |

|

40 |

Murata |

村田 |

PCB |

560 |

|

41 |

Dynamic |

定颖电子 |

PCB |

528 |

|

42 |

Shenyi Electronics |

生益电子 |

PCB |

525 |

|

43 |

APEX Intermatona |

泰鼎 |

PCB |

514 |

|

44 |

Career Technoogy |

嘉联益 |

FPC |

508 |

|

45 |

Founder PCB |

方正 |

PCB |

500 |

|

46 |

ISU-Petasys |

梨树 |

PCB |

498 |

|

47 |

Sun & Lynn |

深联电路 |

PCB+FPC+ |

495 |

|

48 |

Kyocera PCB |

京瓷 |

PCB |

495 |

|

49 |

KCE Electronics |

KCE |

PCB |

483 |

|

50 |

Gul Technologies |

高德 |

PCB |

478 |

|

51 |

CEE PCB |

中京电子 |

PCB |

454 |

|

52 |

Eilington |

依顿 |

PCB |

454 |

|

53 |

WuZhou |

五株科技 |

PCB+FPC |

441 |

|

54 |

CCTC |

汕头超声 |

PCB |

440 |

|

55 |

Bomin |

博敏电子 |

PCB |

433 |

|

56 |

Hongxin Electronics |

厦门弘信电子 |

FPC |

415 |

|

57 |

Kyoden |

京电 |

PCB |

399 |

|

58 |

Guangdong Kingshine |

广东科翔 |

PCB |

392 |

|

59 |

Guangzhou Jun Ya |

广东骏亚 |

PCB |

382 |

|

60 |

Sanmina |

新美亚 |

PCB |

340 |

|

61 |

Redboard |

红板 |

PCB+HDI |

327 |

|

62 |

Lincstech |

Lincstech |

PCB |

327 |

|

63 |

SI flex |

世一 |

PCB |

315 |

|

64 |

Taihong Circuit industry |

台虹 |

PCB |

309 |

|

65 |

Transtech |

江苏偿苣 |

- |

297 |

|

66 |

Shenzhen Sunshine |

深圳明阳电路 |

PCB |

292 |

|

67 |

Guangdong XD Group |

佳康集团 |

- |

290 |

|

68 |

FICT |

FICT |

PCB |

282 |

|

69 |

MFS |

湖南维胜 |

FPC+PCB |

281 |

|

70 |

Delton Technolagy |

广合科技 |

PCB+HDI |

280 |

|

71 |

Ichia Technology |

毅嘉科技 |

PCB |

264 |

|

72 |

DAP |

DAP |

PCB |

256 |

|

73 |

Shirai Denshi |

日本日开 |

PCB |

250 |

|

74 |

ACCESS |

珠海越亚 |

PCB |

249 |

|

75 |

STEMCO |

STEMCO |

PCB |

244 |

|

76 |

APCB |

竞国 |

FPC |

240 |

|

77 |

Haesung DS |

Haesung Ds |

PCB |

234 |

|

78 |

sZ Jove Enterprise |

中富电路 |

PCB |

228 |

|

79 |

Daisho Denshi |

大昌微线 |

PCB+HDI |

228 |

|

80 |

Wurth Elektronic |

伍尔特 |

PCB |

224 |

|

81 |

Camelot PCB |

金禄电路 |

PCB |

222 |

|

82 |

Onpress |

安柏电路 |

PCB |

218 |

|

83 |

Summit Interconnec |

Summit Interconnec |

FPC |

200 |

|

84 |

Somacis |

Somacis |

FPC+PCB |

200 |

|

85 |

Kunshan Huaxing Grp |

昆山华新 |

PCB |

197 |

|

86 |

Guangzhou GCI |

广州杰赛 |

PCB |

196 |

|

87 |

Kyosha |

京写电路 |

PCB |

186 |

|

88 |

Jia LiChuang |

先进电子(珠海) |

PCB |

183 |

|

89 |

Shihui Fushi |

四会富任电子科技 |

PCB |

181 |

|

90 |

Amphenol PCB |

安费诺 |

FPC |

180 |

|

91 |

Jiangxi ZLE |

江西中络 |

PCB |

177 |

|

92 |

Liang Dar |

良达科技 |

PCB |

174 |

|

93 |

TLB |

TLB |

- |

172 |

|

94 |

Changzhou Auhong |

常州澳弘电子 |

PCB |

171 |

|

95 |

Glorysky |

惠州市特创电子 |

PCB |

171 |

|

96 |

Leader-Tech |

上达电子 |

FPC |

164 |

|

97 |

Minzhenhong |

明正宏电子 |

PCB |

163 |

|

98 |

Dongguang Hongyuen |

东莞康源电子 |

PCB |

163 |

|

99 |

New Flex |

New Flex |

- |

163 |

|

100 |

Hyumwoo |

Hyumwoo |

- |

162 |

Source: NTI, compiled by Bossonresearch

Key Points and Facts:

Global PCB Factory Overview:

Approximately 2,800 PCB factories worldwide.

116 factories generate over $100 million in annual revenue.

Major production hubs: United States, Japan, South Korea, mainland China, Taiwan.

Top 100 PCB Companies:

Combined revenue of the top 100 companies: $81.99 billion.

All top 100 companies generate over $100 million annually in PCB production.

Top 10 Global PCB Companies (by revenue): ZD Tech, Unimicron, DSBJ, Compeq, Nippon Mektron, TTM Technologies, Trpod, Nanya PCB, Shennan Circuit, Ibiden.

Chinese companies in Top 10: 7 out of the top 10, with 2 mainland Chinese (DSBJ and Shennan circuit) and 5 Taiwanese (ZD Tech, Unimicron, Compeq, Trpod, and Nanya PCB).

Other countries in Top 10: 2 Japanese (Ibiden, Nippon Mektron) and 1 U.S. (TTM Technologies).

Asia-Centered PCB Industry:

Mainland China dominates the global PCB industry.

China's share of global PCB production value surged from 8.1% in 2000 to 56.0% in 2024.

China is now the undisputed global leader in PCB manufacturing.

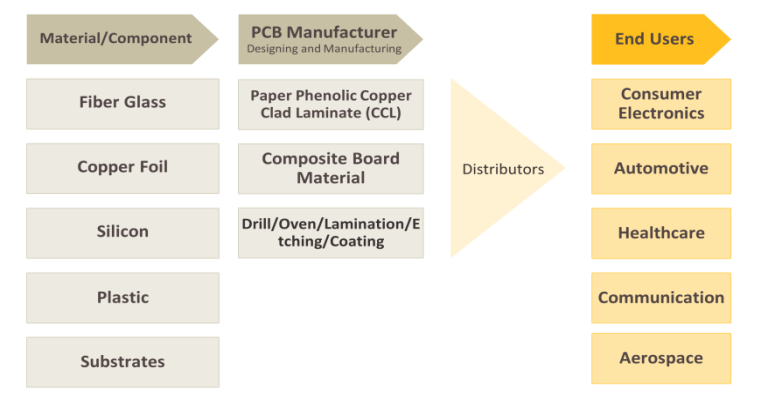

PCB Industry Chain Analysis

(1) Upstream:

The upstream of the PCB industry chain involves raw materials, with direct material costs accounting for about 55% of total costs. Among these, copper-clad laminate (CCL) materials account for over 30%, copper foil for approximately 9%, steel balls for around 6%, and gold salt ink and other materials for about 3%. Fluctuations in the price of copper-clad laminate have a significant impact on midstream PCB manufacturers. The three main raw materials for copper-clad laminate are copper foil, resin, and glass fiber cloth, which are the primary substrates for achieving conductivity, insulation, and support in PCBs, with cost proportions of 42%, 26%, and 19%, respectively. Price fluctuations in copper-clad laminate materials significantly affect costs. Specifically, copper foil prices depend on changes in copper prices, which are greatly influenced by international steel prices, while glass fiber cloth prices are more affected by supply and demand dynamics.

(2) Midstream:

To adapt to global supply chain development trends and the growing demand for high-end products, PCB production capacity expansion is mainly progressing in two directions:

Southeast Asia Investment and Factory Setup: According to data from the Taiwan Printed Circuit Association (TPCA), Southeast Asia is becoming a key beneficiary of the global PCB and electronic supply chain. Taiwanese PCB manufacturers, such as Unimicron, Compeq, Gold Circuit Electronics, and Zhen Ding Technology, are actively expanding into Thailand. In 2023, Thailand's PCB production value accounted for about 3.8% of the global total. With continued investment from manufacturers, it is expected to grow to 4.7% by 2025.

Production of High-End Packaging Substrates: Packaging substrates benefit from technological upgrades and expanded application scenarios, such as artificial intelligence, cloud computing, intelligent driving, and the Internet of Things. These developments have significantly driven the growth in demand for high-end chips and advanced packaging, leading to long-term growth in the global packaging substrate industry. This is particularly evident in the rapid growth of high-end packaging substrates for high computing power and integration scenarios.

(3) Downstream:

PCBs are widely used in traditional fields such as communication, computers, and home appliances. In terms of specific application sectors, communication, computers, consumer electronics, and automotive electronics are the top four downstream applications, together accounting for nearly 90% of the market. The prosperity of these sectors directly influences the market conditions of the PCB industry. Downstream terminal brands are relatively more concentrated compared to PCB manufacturers, which means that PCB manufacturers have relatively weaker pricing power.

About US:

Bosson Research (BSR) is a leading market research and consulting company, provides market intelligence, advisory service and market research reports for the automobile, electronics and semiconductor, and consumer good industry. The company assists its clients to strategize business policies and achieve sustainable growth in their respective market domain.

Bosson Research provides one-stop solution right from data collection to investment advice. The analysts at Bosson Research (BSR) dig out factors that help clients understand the significance and impact of market dynamics. Bosson Research (BSR) bring together the deepest intelligence across the widest set of capital-intensive industries and markets. By connecting data across variables, our analysts and industry specialists present our customers with a richer, highly integrated view of their world.

Contact US:

Tel: +86 400-166-9288

E-mail: sales@bossonresearch.com